Abstract

In this paper, reliability properties of a system that is subject to a sequence of shocks are investigated under a particular new change point model. According to the model, a change in the distribution of the shock magnitudes occurs upon the occurrence of a shock that is above a certain critical level. The system fails when the time between successive shocks is less than a given threshold, or the magnitude of a single shock is above a critical threshold. The survival function of the system is studied under both cases when the times between shocks follow discrete distribution and when the times between shocks follow continuous distribution. Matrix-based expressions are obtained for matrix-geometric discrete intershock times and for matrix-exponential continuous intershock times, as well.

Similar content being viewed by others

1 Introduction

Although the event of system failure is defined through the magnitudes of random shocks in classical shock models, according to the delta shock model, the system fails if the length of the times between two successive shocks is less than a given fixed threshold. Such a model has been studied by Li (1984), Li and Kong (2007), Li and Zhao (2007) when the shocks occur according to a Poisson process, i.e. the interarrival times between shocks are exponentially distributed. Tuncel and Eryilmaz (2018) obtained the survival function and the mean time to failure of the system when intershock times follow proportional hazard rate model. Eryilmaz (2017) studied reliability properties of a system under the delta shock model when the shocks occur according to a Polya process. Under the assumption of Polya process, the interarrival times between successive shocks are no longer independent.

Various modifications and generalizations of delta shock (or simply, \(\delta\)-shock) models have been introduced to represent real life systems and processes. Mallor and Santos (2003) studied a general shock model that generalizes the extreme, the cumulative and the run shock models. Wang and Zhang (2005) defined a mixed shock model. According to their model, the system fails if either the time between two successive shocks is less than a given threshold or the magnitude of a single shock exceeds a given threshold. This is a mixed model that combines delta and extreme shock models. See also Parvardeh and Balakrishnan (2015) for mixed shock models. Eryilmaz (2012) extended the delta shock model to the case when the system fails if a specified number of consecutive interarrival times are less than a threshold delta. Jiang (2020) defined and studied a generalized delta shock model with multi-failure thresholds. Goyal et al. (2022a) introduced a general δ-shock model when the recovery time depends on both the arrival times and the magnitudes of shocks. See also Lorvand et al. (2019), Poursaeed (2021), Goyal et al. (2022b) and Lorvard and Nematollahi (2022) for other types of extensions and generalizations of the delta shock model.

Shock models have wide applications for modeling various real-life processes and systems. The term shock is generic, and it can be replaced by an appropriate concept depending on the process under concern. For example, in a certain spare parts inventory management system, demands arrive randomly with random size. In this case, the interarrival times are the times between successive demands. The size of a demand coincides with the magnitude of a shock. In a certain portfolio of an insurance company, claims occur randomly over time. In this case, the interarrival times are the times between successive claims and the magnitudes of the shocks are the sizes of the claims.

In most real-life situations, after a shock that is above a certain level, the characteristics, e.g., distribution of the shocks may change. For example, if the shock is a kind of environmental effect, e.g., pressure, temperature, and wind, then a harsher environment might be available after the shock that is significantly different from the previous shocks. Eryilmaz and Kan (2021) studied reliability and optimal replacement policy for an extreme shock model when the distribution of the shock size changes after a random number of shocks following a particular distribution. In particular, for a sequence of shock sizes denoted by \(Y_{1}\), \(Y_{2}\), \(\cdots\), they considered the case when \(Y_{1}\), \(Y_{2}\), \(\cdots\), \(Y_{M}\) are independent and identically distributed (iid) with common distribution \(G_{1}\) and \(Y_{M + 1}\), \(Y_{M + 2}\), \(\cdots\) are iid with common distribution \(G_{2}\), where \(M\) is a positive discrete random variable independent of \(Y_{i}\)’s and follows a particular distribution. Also, Eryilmaz and Kan (2021), studied the reliability of an extreme shock model when there is a change in the shock size distribution. According to their model, the change in shock size distribution occurs upon the occurrence of a shock that is above a fixed warning threshold. They assumed that the distribution of the magnitudes of shocks changes after the first shock of size at least \(d_{1}\) a given level. That is, if \(N_{{d_{1} }}\) denotes the number of shocks until the first shock of size at least \(d_{1}\), then it is assumed that \(Y_{1}\), \(Y_{2}\), \(\cdots\), \(Y_{{N_{{d_{1} }} }}\) have common distribution \(G_{1}\), and \(Y_{{N_{{d_{1} }} + 1}}\), \(Y_{{N_{{d_{1} }} + 2}}\), \(\cdots\) have another common distribution \(G_{2}\). In this case, the random variable \(N_{{d_{1} }}\) denotes the number of shocks until the change point depends on \(Y_{1}\), \(Y_{2}\), \(\cdots\). Applications of this model to statistical control processes and wind turbines are given by Eryilmaz and Kan (2021).

In this paper, we study a new mixed shock model that combines extreme and delta shock models under the change point model proposed by Eryilmaz and Kan (2021). Such a model is useful for modeling various real-life systems or processes. In general, this proposed new change point setup is useful to model the situation when there is a change in behavior of the system/process upon the occurrence of an unexpected event, e.g., a sudden change in environmental condition, a large claim due to an extreme event, an enormous demand shock for health care systems and ventilators due to COVID-19. Such changes ensure the change in probability distribution of the shock/claim/demand. Also, this model is useful for insurance portfolio management. Consider a heterogeneous portfolio of losses and/or payments of an insurance company. Expected losses are defined by a threshold, say \(d_{1}\), and are such that the loss sizes do not exceed the threshold \(d_{1}\). An unexpected future loss, (with loss size exceeding the value of the threshold) could be used as a warning for an approaching high-risk situation for the portfolio since the distribution of the claim sizes may change after an unexpected loss. This may occur if the portfolio is affected by a random event such as explosion, breakdown that influence all policies. A plausible criterion to confer that a high-risk situation is approaching for the insurance company would be to observe at least two unexpected losses that are very close to each other or more generally to observe least two unexpected losses which are separated by at most \(\delta\) expected losses (this corresponds to the classical \(\delta\)-shock model) as well as the size of a unexpected catastrophic loss is at least \(d > d_{1}\) (this corresponds to the extreme shock model).

The findings of the paper can be summarized as follows:

-

The probability generating function (Laplace-Stieltjes transform) of the system’s lifetime is obtained when the times between shocks follow discrete (continuous) distribution

-

The matrix-based expressions for the survival function of the system are obtained when the times between shocks follow discrete matrix-geometric (continuous matrix-exponential) distribution.

In mixed shock models, system failure results from the competing failure criteria. Indeed, in most real-life processes, the system failure occurs with respect to the occurrence of two or more different events. The novelty of the present paper lies in combining the mixed shock model previously studied in the literature with the change point-based model. Such a combined model is flexible and can be used in a more general setting.

The paper is organized as follows. In Sect. 2, the model is described, and some preliminary results are presented. In Sect. 3, the reliability properties of the system are investigated under both cases when the interarrival times between successive shocks follow discrete and continuous probability distributions. Section 4 contains numerical illustrations.

2 Description of the model and preliminary results

We consider a system that is subject to random shocks. Let \(X_{1}\), \(X_{2}\), \(\cdots\) be the interarrival times between successive shocks, with common distribution function (df) \(F\left( x \right) = 1 - \overline{F}\left( x \right) = {\text{Pr}}\left( {X \le x} \right)\), where \(X\) denotes a generic random variable of \(X_{i}\) s. Also, let \(Y_{1}\), \(Y_{2}\), \(\cdots\) be the random magnitudes of the shocks. It is assumed that the distribution of the magnitudes of shocks changes after the first shock of size at least \(d_{1} > 0\). That is, the random shock magnitudes \(Y_{1}\), \(Y_{2}\), \(\cdots\), \(Y_{{N_{{d_{1} }} }}\) have common df \(G_{1}\), and \(Y_{{N_{{d_{1} }} + 1}}\), \(Y_{{N_{{d_{1} }} + 2}}\), \(\cdots\) have common df \(G_{2}\), where \(N_{{d_{1} }}\) denotes the random number of shocks until the first shock of size at least \(d_{1}\). The system fails when the time between successive shocks is less than a given threshold \(\delta > 0\), or the magnitude of a single shock is at least \(d\), where \(d > d_{1}\). Let also \(N_{d}\) denotes the number of shocks for which the time between successive shocks is less than a given threshold \(\delta\), or the magnitude of a single shock is at least \(d\). Then, the lifetime of the system is \(T = \mathop \sum \limits_{i = 1}^{{N_{d} }} X_{i}\), Hence, \(T\) is a random sum and has a compound distribution.

For simplicity, let us denote by:

\(p_{1} = G_{1} \left( {d_{1} } \right)\): the probability that the magnitude of a shock before the change in shock size distribution is below \(d_{1}\),

\(p_{2} = G_{1} \left( d \right)\): the probability that the magnitude of a shock before the change in shock size distribution is below \(d\),

\(p_{3} = G_{2} \left( d \right)\): the probability that the magnitude of a shock after the change in shock size distribution is below \(d\).

It should be noted that the mixed shock model considered in the present paper coincides with the model studied by Eryilmaz and Kan (2021) when \(\delta \to 0\).

In the following Lemma 1 we obtain the joint probability mass function (pmf) of the random vector \((N_{{d_{1} }}\), \(N_{d} )\).

Lemma 1.

The joint pmf of the random variables \(N_{{d_{1} }}\) and \(N_{d}\) is

Proof.

For \(n > m\) we have

and

For \(n = m\) we have

and

\(\square\)

Using Lemma 1, we can easily obtain the marginal pmfs of the random variables \({N}_{{d}_{1}}\) and \({N}_{d}\), given in the following:

Corollary 1.

(i) The marginal pmf of \({N}_{{d}_{1}}\) is given by.

(ii) The marginal pmf of \(N_{d}\) is given by

for \(p_{1} \ne p_{3}\) , and

for \(p_{1} = p_{3}\) .

Proof.

(i) Using (1) we get

(ii) Similarly, from (1) we obtain

Now, the result follows immediately, since

\(\square\)

Remark 1. (i) From Eq. (2), we have that the random variable \(N_{{d_{1} }}\) follows the geometric distribution with parameter \(1 - p_{1} \overline{F}\left( \delta \right)\).

(ii) Let \(p_{1} \ne p_{3}\).

Let also

and consider the geometric random variables \(W_{1}\) and \(W_{2}\) having probability mass functions

and

respectively. Note that \(W_{1} \triangleq N_{{d_{1} }}\), where the symbol \(\triangleq\) means equality in distribution.

Then Eq. (3) can be rewritten as

Therefore, the distribution of the random variable \(N_{d}\) is a mixture of two geometric distributions. It should be noted that the weights \(\omega\) and \(1 - \omega\) may take negative values and hence, Eq. (8) is a generalized mixture of two geometric distributions.

(iii) Let \(p_{1} = p_{3}\).

Then, Eq. (4) can also be rewritten as

where

\(\Pr \left( {W_{2} = n} \right)\) is given by (7), and the random variable \(U_{1}\) has the negative binomial distribution with probability mass function

Therefore, since the weights \(\theta\) and \(1 - \theta\) may take negative values, Eq. (9) is a generalized mixture of negative binomial and geometric distributions.

3 Reliability of the system

For our system, the following two dependent lifetime random variables are of interest

Note that \({T}_{1}\) and \(T\) are compound random variables (or random sums), \({T}_{1}\) denotes the time until the first shock is of size at least \({d}_{1}\), i.e., it is the time until the change point and the random variable \(T\) denotes the lifetime of the system.

In the sequel, we examine two cases according to which the interarrival times \({X}_{1}\), \({X}_{2}\), \(\cdots\) between successive shocks have a discrete or a continuous distribution.

3.1 The discrete case

Suppose that the interarrival times \({X}_{1}\), \({X}_{2}\), \(\cdots\) between successive shocks have a discrete distribution with an arbitrary common df \(F\). Let \(f\left(t\right)=\mathrm{Pr}(X=t)\) be the pmf of \(X\) and \({f}_{T}\left(t\right)=\mathrm{Pr}(T=t)\) be the pmf of the lifetime \(T\). Define the probability generating functions (pgf) of the conditional random variables \(X\left|X\le \delta \right.\) and \(X\left|X>\delta \right.\) by

and

Then, we have the following.

Theorem 1.

Let \(P_{{T_{1} ,T}} \left( {u_{1} ,u} \right) = E\left[ {u_{1}^{{T_{1} }} u^{T} } \right]\) be the joint pgf of the random vector \(\left( {T_{1} , T} \right)\) . Then, it holds.

Proof.

By conditioning on \(\left( {N_{{d_{1} }} , N_{d} } \right)\) we get

The result follows using the details in the proof of Lemma 1. \(\square\)

By letting \(u = 1 {\text{and}}\) \(u_{1} = 1\) in Theorem 1 we obtain the marginal pgfs of the lifetimes \(T_{1} and\) \(T,\) respectively. Thus, we have the following:

Corollary 2.

(i) The pgf \(P_{{T_{1} }} \left( u \right) = E\left[ {u^{{T_{1} }} } \right]\) of the lifetime random variable \(T_{1} is\).

(ii) The pgf \(P_{T} \left( u \right) = E\left[ {u^{T} } \right]\) of the lifetime random variable \(T\) is

Using that \(E\left[ {T_{1} } \right] = P_{{T_{1} }}^{^{\prime}} \left( 1 \right)\) and \(E\left[ T \right] = P_{T}^{^{\prime}} \left( 1 \right)\) and Corollary 2, we can obtain the means of the random variables \(T_{1}\) and \(T\). Thus, we have the following:

Corollary 3.

The mean of \(T_{1}\) is

and the mean time to failure (MTTF) of the system is

For some specific distributions of the random variable \(X\) we can obtain analytical results for the evaluation of the distributions of the lifetime random variables \(T_{1}\) and \(T\).

At first, we consider the particular case when the interarrival times between successive shocks follow the geometric distribution with common pmf

and we represent the random variables \(T_{1}\) and \(T\) as matrix-geometric distributions.

A discrete random variable \(W\) with zero pmf at zero that has a probability generating function in the form

for some \(m \ge 1\) and real constants \(c_{1} , \ldots ,c_{m}\) and \(d_{1} , \ldots ,d_{m}\), is said to have a matrix-geometric distribution (see, e.g. Bladt and Nielsen (2017)). In this case, the probability mass function and the survival function of the random variable \(T_{\delta }\) can be represented, respectively, as

and

where \({\varvec{\pi}} = \left( {1,0, \ldots ,0} \right)\) is a \(1 \times m\) row vector, \({\varvec{I}}_{m}\) is the identity matrix of order \(m\), and the \(m \times m\) matrix \({\varvec{Q}}\) and the \(m \times 1\) column vector \({u^{\prime}}\) are given by

We write \(W\sim MG_{m} \left( {{\varvec{Q}}, {\varvec{u}}} \right)\), to represent that the random variable \(W\) has matrix-geometric distribution.

Theorem 2.

Let the interarrival times between successive shocks follow the geometric distribution with common pmf given by (14). Then

(i) The random variable \(T_{1} \sim MG_{\delta + 1} \left( {{\varvec{Q}}, {\varvec{u}}} \right)\), where \({\varvec{Q}}\)\(:\delta + 1 \times\) \(\delta + 1\) and \({u^{\prime}}\)\(:\delta + 1 \times 1\) are given by (18) with

(ii) The random variable \(T\sim MG_{2\delta + 2} \left( {{\varvec{Q}}, {\varvec{u}}} \right)\), where \({\varvec{Q}}\)\(:2\left( {\delta + 1} \right) \times 2\left( {\delta + 1} \right)\) and \({u^{\prime}}\)\(:2\left( {\delta + 1} \right) \times 1\) are given by (18) with

Proof.

Under the assumptions of the Theorem,

and

(i) Using Eq. (12), the pgf of \(T_{1}\) is obtained as

and hence the result follows directly from (15).

(ii) Using Eq, (13), the pgf of \(T\) can be written as

where the coefficients \(c_{i}\) and \(d_{i}\) are as given in the theorem. Since \(P_{T} \left( u \right)\) is of the form of Eq. (15), the result follows immediately. \(\square\)

3.2 The continuous case

Now suppose that the interarrival times \(X_{1}\), \(X_{2}\), \(\cdots\) between successive shocks have a continuous distribution with an arbitrary common df \(F\left( t \right) = {\text{Pr}}\left( {X \le t} \right)\) and let \(f\left( t \right) = F^{\prime}\left( t \right)\) denotes its common probability density function (pdf). Also, let \(\hat{f}\left( u \right) = E\left[ {e^{ - uX} } \right] = \mathop \smallint \limits_{0}^{\infty } e^{ - ut} f\left( t \right)dt\) be the Laplace–Stieltjes transform (LST) of \(X\). Similar to the proof of Theorem 2, we can obtain the joint LST \(\hat{f}_{{T_{1} , T}} \left( {u_{1} , u} \right) = E\left[ {e^{{ - u_{1} T_{1} - uT}} } \right]\) of the random vector \(\left( {T_{1} , T} \right)\) given in the following Theorem 3. Define the LSTs of the random variables \(X\left| {X \le \delta } \right.\) and \(X\left| {X > \delta } \right.\) by

and

respectively, then we have the next.

Theorem 3.

The joint LST \(\hat{f}_{{T_{1} , T}} \left( {u_{1} , u} \right) = E\left[ {e^{{ - u_{1} T_{1} - uT}} } \right]\) of the random vector \(\left( {T_{1} , T} \right)\) is.

Using the LST of Theorem 3, we get the marginal LSTs \(\hat{f}_{{T_{1} }} \left( u \right) = E\left[ {e^{{ - uT_{1} }} } \right]\) and \(\hat{f}_{T} \left( u \right) = E\left[ {e^{ - uT} } \right]\) of the random variables \(T_{1}\) and \(T\).

Corollary 4.

The marginal LSTs corresponding to \(T_{1}\) and \(T\) are given, respectively, by.

and

It should be noted that using the relations \(E\left[ {T_{1} } \right] = - \hat{f}_{{T_{1} }}^{^{\prime}} \left( 0 \right)\), \(E\left[ T \right] = - \hat{f}_{T}^{^{\prime}} \left( 0 \right)\) and Corollary 4, we can obtain the means of the random variables \(T_{1}\) and \(T\). Their expressions are the same with those given in Corollary 3 for the discrete case.

As in the discrete case, by considering specific distributions of the random variable \(X\), we can obtain analytical results for the evaluation of the distributions of the lifetime random variables \(T_{1}\) and \(T\). We consider the particular case when the interarrival times between successive shocks follow the exponential distribution with common pdf

In this case, we have

and

Using Corollary 3, the LSTs of the random variables \(T_{1}\) and \(T\) are found to be

and

Corollary 5

Let \(X_{i}\) have the exponential distribution with parameter \(\lambda > 0\). If \(\delta \to \infty\), then the distribution of the random variables \(T_{1}\) and \(T\) approaches the exponential distribution with parameter \(\lambda\), that is.

Proof.

The result follows immediately from (19) and (20), since

and \(\lambda /\left( {\lambda + u} \right)\) is the LST of the exponential distribution with parameter \(\lambda\). \(\square\)

A continuous random variable \(W\) is said to have a matrix-exponential distribution, if its distribution function is given by

where \({\varvec{a}}\) is a \(p \times 1\) vector, \({\varvec{S}}\) is a \(p \times p\) matrix (which is called a companion matrix) and \({\varvec{s}}\) is a \(p \times 1\) vector. We write \(W\sim ME_{p} (\user2{a,S,s}),\) to present that the random variable \(W\) has a matrix-exponential distribution with parameters \((\user2{a,S,s})\). The common probability density function is computed from \(f_{W} \left( t \right) = {\varvec{a}}^{T} exp\left( {{\varvec{S}}t} \right){\varvec{s}}\). If \(\hat{f}_{W} \left( u \right) = E\left[ {e^{ - uX} } \right] = \mathop \smallint \limits_{0}^{\infty } e^{ - ut} f\left( t \right)dt\) denotes the Laplace–Stieltjes transform of \(X\), then \(\hat{f}_{W} \left( u \right) \) can be computed from

where \({\varvec{I}}_{p}\) is the identity matrix of order \(p\).

The non-centralized moments of \(W\) can be computed from

Asmussen and Bladt (1997) showed that if \(W\sim ME_{p} ({\varvec{a}}\), \({\varvec{S}}\), \({\varvec{s}})\), then the LST \(\hat{f}_{W} \left( u \right)\) is rational and can be written as

where \(a_{i}\), \(b_{i}\), \(1 \le i \le n\) are real numbers. It should be noted that Eq. (22) holds true when there is no point mass at zero. Then, the representation \(({\varvec{a}}\), \({\varvec{S}}\), \({\varvec{s}})\) is given by

For a comprehensive review of matrix-exponential distributions and their sub-class of phase-type distributions, we refer to Bladt and Nielsen (2017).

As it is clear from (19) and (20), the LSTs of the random variables \(T_{1}\) and \(T\) are not in the form of (22). That is, the numerator and denominator are not polynomial functions. Therefore, the random variables \(T_{1}\) and \(T\) do not have matrix-exponential distributions. However, using the Taylor expansion for the exponential terms involved in (19) and (20), the LSTs and hence the survival functions of \(T_{1}\) and \(T\) can be approximated by matrix-exponential distributions. Such a method has been used by Kus et al. (2022) and Chadjiconstantinidis and Eryilmaz (2022). To obtain the approximated values of the survival functions, we first represent (19) and (20) in the form of (22) via Taylor expansion of the exponential terms and then use (23).

For illustration purposes, let us consider the LST of the random variables \(T_{1}\). Multiplying both the numerator and the denominator of the right-hand side of (19) by \(e^{u\delta }\), we get

For sufficiently large \(q\), using the Taylor expansion \(\mathop \sum \limits_{i = 0}^{q - 1} \frac{{\left( {\delta u} \right)^{i} }}{i!}\) for the term \(e^{\delta u}\) the LST of \(T_{1}\) can be approximated by the rational LST

where

Therefore, the approximated random variable \(\tilde{T}_{1}\) of \(T_{1}\) has a matrix-exponential distribution, and hence, using these coefficients, the survival function of \(T_{1}\) can be approximated by

where

and \(b_{i}\)’s, \(a_{i}\)’s are given as above.

By a similar way, using (20) we can approximate the LST of \(T\) by a rational LST, and hence we can approximate the distribution of \(T\) by a matrix-exponential distribution. Using Corollary 4, this approach can be easily applied and for the more general case when the interarrival times between successive shocks have a matrix-exponential distribution. The details are omitted (see, for example in Kus et al. (2022) and Chajiconstantinidis and Eryilmaz (2022)).

4 Numerical illustrations

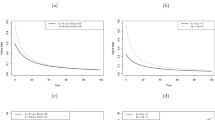

In this section, we present some illustrative computational results. First, consider the case when the intershock times follow the geometric distribution with mean \(\frac{1}{p}\) and when \(\delta =2\) and \({p}_{1}=0.7,{p}_{2}=0.9,{p}_{3}=0.6\). In Table 1, we present the survival functions of \({T}_{1}\) and \(T\) for selected values of \(t\). Clearly, the survival functions are decreasing in \(p\) since we expect more frequent shocks with an increase in \(p\).

Table 2 contains approximated values of the survival functions when the intershock times have exponential distribution with mean \(\frac{1}{\lambda }\) when \({{p}_{2}=0.9, p}_{3}=0.6\) and \(\delta =2\). As expected, an increase in \(\lambda\) leads to a decrease in survival probabilities.

5 Reliability application

Kus et al. (2022) used the mixed \(\delta\)-shock model to represent a repairable system consisting of active and cold standby components. As noted by Kus et al. (2022), at time t = 0, both of the components are new, and component 1 starts operation first, while component 2 is in a cold standby state. The standby component is switched into operation when the active component (component 1) fails, and a repair action is immediately taken for component 1. Suppose that the repair time for a failed component is fixed as δ, and the component is as good as new after repair. A damage of random size occurs upon the failure of a component. Let \({Y}_{i+1}\) denote the magnitude of the damage for the component who lives\({X}_{i}\), i = 0, 1, 2, …. If the size of the damage is above d, then the unit cannot be repaired and hence the system fails after the failure of the standby component. Such a repairable system fails either if one of \({X}_{i}\) s is less than or equal to δ or the size of the damage for a failed component is above d. The lifetime of the system is then represented as

Under the change point setup considered in the present paper, the random variable \({N}_{{d}_{1}}\) denotes the number of component failures until the first damage that is at least \({d}_{1}.\) Assume that the size of the damage is determined by a certain environmental factor. Thus, the probabilistic law of the damage size changes after the damage above the threshold \({d}_{1}\).

Suppose that there is a desired level for the mean time to failure (MTTF) of the system. If the MTTF of the system is below a given specified level, then an additional standby component may be added to increase the performance of the system. The MTTF of the system can be computed from

where \(F\left(x\right)=\mathrm{Pr}(X\le x)\) is the time to failure distribution of the component. The distribution \(F\left(x\right)\) may be either discrete or continuous depending on the system. If the lifetime of the component corresponds to the number of cycles, then \(F\left(x\right)\) should be modeled as discrete. For example, the lifetimes of batteries may be measured in terms of how many times their charge–discharge processes have been repeated. In this case, a cycle is one complete use of the battery to store power and release it (Willis and Scott (2000)).

6 Summary and conclusions

In this paper, a mixed shock model that combines extreme and delta shock models has been studied when there is a change in shock size distribution. Computationally efficient matrix-based expressions were obtained for the survival function and mean time to failure of the system. The results extend and generalize the previous results mainly in two directions. First, the model of Eryilmaz and Kan (2021) has been extended to a mixed model. Second, discrete intershock times have also been considered for reliability evaluation of the system. The latter one is also new for the extreme shock model with a change point studied in Eryilmaz and Kan (2021). As a future work, more general models and extensions can be considered. For example, a mixed model that combines run and delta shock models can be studied. The dependence between shock magnitude and the intershock time may be considered as well. The consideration of the change point in the interarrival times is also worthy to investigate since it is applicable to real life systems.

References

Asmussen S, Bladt M (1997) Renewal theory and queueing algorithms for matrix-exponen-tial distributions. In: Alfa A, Chakravarthy SR (eds) Matrix-analytic methods in stochastic models. Taylor and Francis, Boca Raton, pp 313–341

Bladt M, Nielsen BF (2017) Matrix-exponential Distributions in Applied Probability. Springer, New York

Chadjiconstantinidis S, Eryilmaz S (2022) Reliability assessment for censored δ-shock Models. Methodol Comput Appl Probab. https://doi.org/10.1007/s11009-022-09972-z

Eryilmaz S (2012) Generalized δ-shock model via runs. Stat Probab Lett 82:326–331

Eryilmaz S (2017) δ-shock model based on Polya process and its optimal replacement policy. Eur J Oper Res 263:690–697

Eryilmaz S, Kan C (2021) A new shock model with a change in shock size distribution. Probab Eng Inf Sci 35:381–395

Goyal D, Hazra NK, Finkelstein M (2022a) On the general δ-shock model. TEST. https://doi.org/10.1007/s11749-022-00810-5

Goyal D, Hazra NK, Finkelstein M (2022b) On the time-dependent delta-shock model governed by the generalized Polya process. Methodol Comput Appl Probab 24:1627–1650

Jiang Y (2020) A new δ-shock model for systems subject to multiple failure types and its optimal order-replacement policy. Proce Instit Mechan Eng Part O J Risk Reliab 234:138–150

Kus C, Tuncel A, Eryilmaz S (2022) Assessment of shock models for a particular class of intershock time distributions. Methodol Comput Appl Probab 24:213–231

Li ZH (1984) Some distributions related to Poisson processes and their application in solving the problem of traffic jam. J Lanzhou Univ Nat Sci 20:127–136

Li ZH, Kong XB (2007) Life behavior of δ-shock model. Statist Probab Lett 77:577–587

Li ZH, Zhao P (2007) Analysis on the δ-shock model of complex systems. IEEE Trans Reliab 56:340–348

Lorvand H, Nematollahi AR, Poursaeed MH (2019) Life distribution properties of a new delta-shock model. Commun Statist Theory Methods 49:3010–3025

Lorvard H, Nematollahi AR (2022) Generalized mixed delta-shock models with random interarrival times and magnitude of shocks. J Comput Appl Math 403:112832

Mallor F, Santos J (2003) Reliability of systems subject to shocks with a stochastic dependence for the damages. TEST 12:427–444

Parvardeh A, Balakrishnan N (2015) On mixed δ-shock models. Statist Probab Lett 102:51–60

Poursaeed MH (2021) Reliability analysis of an extended shock model. Proce Instit Mech Eng Part O J Risk Reliab 235:845–852

Tuncel A, Eryilmaz S (2018) System reliability under shock model. Commun Statist Theory Methods 47:4872–4880

Wang GJ, Zhang YL (2005) A shock model with two-type failures and optimal replacement policy. Int J Syst Sci 36:209–214

Willis HL, Scott WG (2000) Distributed power generation Planning and Evaluation. CRC Press, Taylor & Francis Group

Acknowledgements

The authors thank the anonymous referees for their helpful comments and suggestions, which were useful in improving the paper.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Chadjiconstantinidis, S., Tuncel, A. & Eryilmaz, S. Α new mixed δ-shock model with a change in shock distribution. TOP 31, 491–509 (2023). https://doi.org/10.1007/s11750-022-00649-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11750-022-00649-x

Keywords

- Delta shock model

- Mixed shock model

- Matrix-geometric distributions

- Matrix-exponential distributions

- Reliability